- Medical costs have tripled in 10 years—₹5 lakh coverage isn't enough anymore

- Super Top-up insurance adds ₹3-10 lakh coverage at 40-50% lower cost than retail options

- Employees pay their own premiums; the company only facilitates (zero cost to employer)

- No waiting periods, covers pre-existing conditions immediately

- Portable across jobs when employees change companies

The ₹5 Lakh Problem Every HR Leader Faces

A senior manager at a Bangalore tech company sent her HR head a panicked message last month. Her mother-in-law needed emergency cardiac surgery. The hospital quoted ₹4.2 lakhs. Her family's group health insurance? ₹5 lakhs for the entire year—covering her, her husband, and two kids.

"What if something happens to my kids later this year?" she asked. "What if my husband needs treatment? We'll be on our own."

The HR head had no good answer.

Ten years ago, a knee replacement surgery cost ₹50,000. Today, the same procedure runs ₹2-2.5 lakhs. Cardiac procedures that were ₹1.5 lakhs are now ₹4-5 lakhs. Cancer treatment that might have cost ₹3-4 lakhs now routinely exceeds ₹10 lakhs.

Medical inflation in India has outpaced almost everything else. But group health insurance coverage? Still stuck at ₹5 lakhs for most companies.

{{divider}}

The math doesn't work anymore:

- Standard GMC coverage: ₹5 lakhs

- Average family size: 4 people

- One major medical event: ₹2-3 lakhs minimum

- Two treatments in a year: Coverage exhausted, family finances exposed

Your employees know this. They're anxious about it. And they're one health crisis away from financial disaster.

{{divider}

Why Doubling Group Health Insurance Coverage Isn't Cost-Effective

Every CHRO knows this conversation by heart. It usually happens during benefits renewal season.

You walk into the CFO's office with a simple request: "We need to increase coverage from ₹5 lakhs to ₹10 lakhs."

The CFO doesn't say no immediately. They open a spreadsheet. They run the numbers. For a company with 500 employees, here's what appears on screen:

The gap: ₹9 lakhs in additional spend.

For a moment, there's silence. The CFO looks at you. You know what they're thinking.

₹9 lakhs is half a senior developer's salary. It's three months of marketing budget for a growing team. It's the difference between making quarterly targets or missing them.

"Can we phase this in next year?" they ask.

But you both know next year, medical costs will be even higher. Premiums will spike again. And the same conversation will repeat—with bigger numbers and tighter budgets.

This isn't a story about a stingy CFO or an unreasonable finance team. It's about the impossible math of medical inflation meeting flat budgets.

Health insurance is already the largest segment of benefits spend.

When you're balancing coverage expansion against hiring needs, product development, and operational costs, something has to give.

Usually, it's employee health coverage.

The hard truth: doubling your benefits budget to fix the coverage gap isn't realistic for most companies. The solution has to come from somewhere else.

{{divider}}

The Alternative That Actually Works: Super Top-Ups

Super Top-up insurance solves the coverage problem without creating a budget problem.

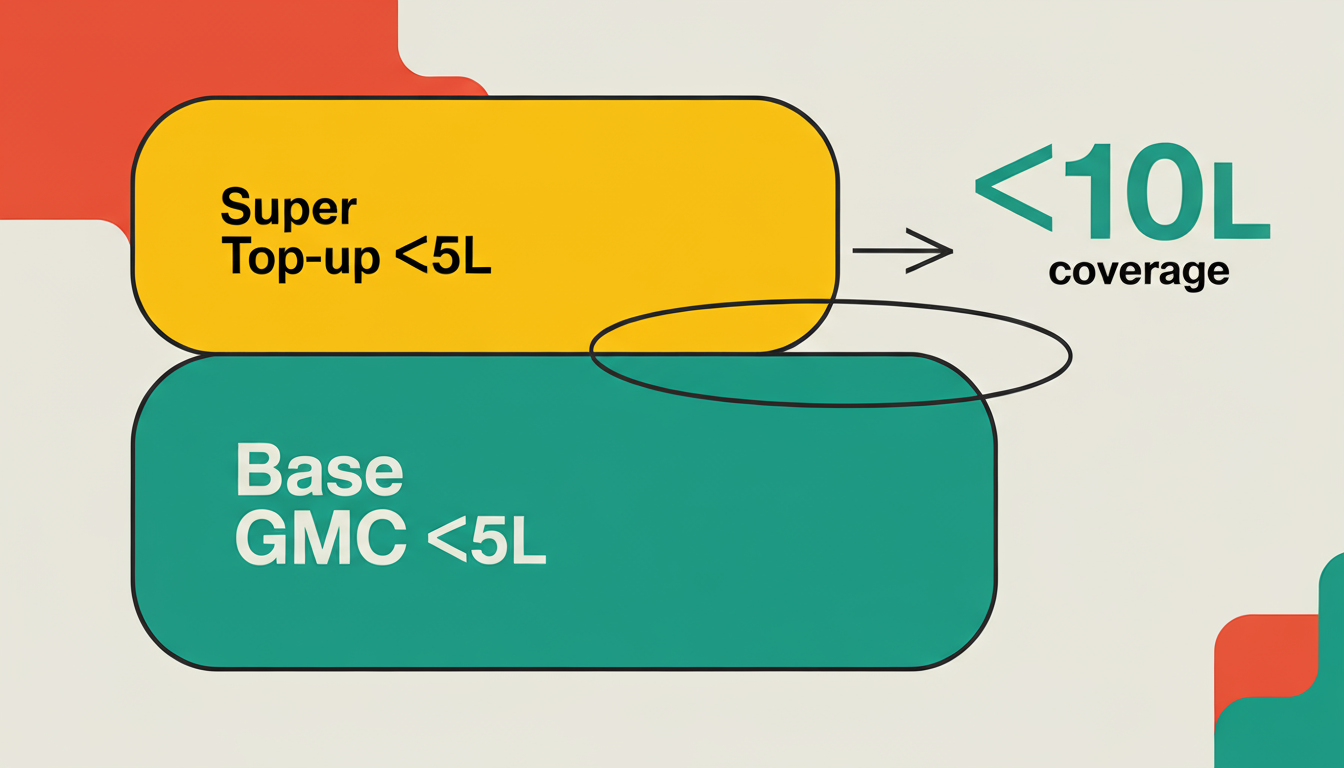

Think of it as a second layer of protection. Your base Group Mediclaim (GMC) covers the first ₹5 lakhs. The Super Top-up kicks in after that, covering the next ₹3-10 lakhs depending on what employees choose.

An employee with a ₹5 lakh base GMC and a ₹5 lakh Super Top-up has a total coverage of ₹10 lakh.

If they have a medical event costing ₹8 lakhs:

- Base GMC pays the first ₹5 lakhs

- Super Top-up pays the remaining ₹3 lakhs

- Employee pays nothing out of pocket

The cost difference is the game-changer.

Increasing base coverage from ₹5L to ₹10L: Company pays ₹9 lakhs extra annually

Adding a ₹5L Super Top-up: Company pays ₹0. Employees pay ₹5,000-7,000 annually for a family of four.

Why is Super Top-up so much cheaper? Because it only activates after the base coverage is used up. The insurance company's risk is lower, so premiums are 40-50% less than retail top-up policies.

Super Top-Up vs Retail Top-Up Insurance: Key Differences

If you've looked at top-up insurance before and dismissed it, you probably looked at retail policies. Super Top-up through a group structure is fundamentally different.

The "replica of GMC" part matters more than it sounds. Whatever your base policy covers—hospitals, treatments, procedures—the Super Top-up covers exactly the same. No separate list of exclusions. No different terms and conditions. No surprises during claims.

This is possible because Super Top-up functions as a direct extension of your existing GMC policy rather than a standalone policy with separate terms. Whatever your base GMC covers today, with no waiting periods, the Super Top-up covers identically once the base limit is exhausted.

{{divider}}

Super Top-Up Implementation: 3 Real Company Examples

Tech Startup, 250 Employees, Bangalore

Average age: 28. Low claims history. CFO nervous about future medical costs as the team ages.

They offered a ₹3 lakh Super Top-up—cost per employee: ₹4,500 annually.

42% of employees signed up. The company spent nothing. The CHRO could now say in interviews: "We offer up to ₹8 lakh in health coverage"—a meaningful differentiator for talent competing with larger companies.

Manufacturing Company, 800 Employees, Pune

Average age: 42. Claims rising 15-20% year over year. CFO had already rejected a ₹20 lakh budget increase to enhance base coverage.

They offered tiered options: a Super Top-up of ₹5 lakh or ₹7.5 lakh. Average cost: ₹7,200 per employee. 38% participation.

The win wasn't just avoiding the ₹20 lakh expense. HR escalations about coverage adequacy dropped 60%. Employees with aging parents or pre-existing conditions had the protection they needed. The company's expense? Still zero.

Retail Chain, 1,200 Employees, Multi-City

High turnover (35% annually). Diverse workforce across 15 cities. Different medical cost structures by region.

They offered a ₹5 lakh Super Top-up with full portability. Cost varied by region: ₹6,000-8,000 per employee.

31% participation—just above the minimum threshold. The portability feature turned out to be the selling point. Employees could keep coverage even after leaving, which reduced anxiety about job changes. In an industry where people switch employers frequently, this mattered.

{{divider}}

How Super Top-Up Portability Works When You Change Jobs

One underrated feature: Super Top-up doesn't vanish when someone changes jobs.

Scenario 1: New company offers equal or better GMC Employee leaves Company A (₹5L GMC) for Company B (₹6L GMC). The Super Top-up transfers seamlessly. No gap in coverage, no paperwork beyond notifying the insurer.

Scenario 2: New company offers lower GMC Employee leaves Company A (₹5L GMC) for a startup offering only ₹3L GMC. Two options:

- Pay the ₹2 lakh difference out of pocket when filing a claim, then Super Top-up covers amounts above ₹5L

- Buy a small retail policy for ₹2 lakhs to bridge the gap, then Super Top-up covers amounts above ₹5L

Scenario 3: Career break or self-employment Employee buys a retail ₹5 lakh base policy. Super Top-up continues covering amounts above that threshold.

This portability matters in India's increasingly mobile workforce. People change jobs every 2-3 years. The idea of "lifetime coverage" built through employer benefits is dead. Portable insurance is the new standard employees expect.

{{divider}}

Super Top-Up Insurance FAQs: Common Questions Answered

- Does the company have to front the money?

In most cases, yes. The insurer invoices the company based on total enrollments. The company pays, then employees reimburse. This is a facilitation payment, not an expense. Most companies either deduct from next month's payroll or allow quarterly installments.

- What happens when someone quits mid-year?

The policy can port to their next employer if the new GMC is equal to or higher. If not, they've still paid for coverage through the policy year. Most companies don't offer prorated refunds to departing employees—too administratively messy for a few months of coverage.

- Is this just pushing costs to employees?

In a sense, yes. But employees get 40-50% better pricing than buying retail on their own, zero waiting periods, and immediate coverage for pre-existing conditions. They're getting more value than they could get independently. And the alternative—company increases base coverage—isn't happening in most organizations due to budget constraints.

- What's the typical cost per employee?

For a family of 4 (self + spouse + 2 children) with ₹5 lakh Super Top-up coverage, annual premiums can vary depending on the employee's age and the insurer's pricing. Younger workforces see lower premiums; older demographics pay slightly more.

{{divider}}

Hidden Benefits of Super Top-Up: Beyond Medical Coverage

Companies that implement Super Top-up report unexpected benefits beyond the coverage itself.

Fewer HR escalations. "My insurance didn't cover this," conversations drop significantly. Employees with adequate coverage don't panic during medical events. They use the insurance and move on.

Better benefits perception. Employees perceive the company as caring about their well-being—even though they're paying the premium themselves. The fact that you facilitated access to better pricing has value.

Less financial stress. No medical debt means no salary advance requests, no distraction from work, no anxiety spirals.

Competitive recruiting advantage. "Enhanced coverage options" become a benefits differentiator without increasing costs. In a tight talent market, non-monetary benefits matter.

Smoother renewals. When base GMC premiums spike 25-30% at renewal, you're not simultaneously fighting to increase coverage limits. Super Top-up has already absorbed that employee demand.

{{divider}}

What This Means for Your 2026 Benefits Strategy

Over the past decade, healthcare has quietly become one of the fastest-inflating costs for employers. In India, treatment expenses for common hospitalizations have more than doubled in just five years, and analysts project a 13% rise in 2025 alone—outpacing salary growth and general inflation by a wide margin.

Globally, the trend is similar, with medical costs climbing around 10% year-on-year for the third straight year.

What’s driving this? More people are seeking treatment, new medical technologies and drugs are pushing prices up, and hospitals are passing on higher operational costs to patients. The result is a structural rise in healthcare spending that’s not going back down anytime soon.

The ₹5 lakh coverage that felt adequate in 2020 leaves employees exposed in 2026. You have three realistic options:

Option 1: Do nothing

Keep ₹5 lakh base coverage. Field escalations when coverage falls short. Hope major medical events don't cluster.

Risk: Employee dissatisfaction, potential medical debt among your workforce, and decreased productivity from financial stress.

Option 2: Increase base coverage

Double your premium expense—typically ₹9-15 lakhs for mid-sized companies. Fight with finance for budget approval. Face premium hikes again next year.

Risk: Budget gets rejected, nothing changes, and employees stay underinsured.

Option 3: Facilitate Super Top-up

Zero additional cost to the company. Employees get 40-50% better pricing than retail. Enhanced coverage without budget battles.

Risk: The Initial effort to communicate the program, and a minimum participation threshold.

The choice isn't complicated. It's just unfamiliar.

Most CHROs haven't encountered employee-funded-but-company-facilitated benefits before. It feels strange at first. But it's increasingly common as medical inflation outpaces corporate budgets.

Here's the reality: Finance teams want to provide better health coverage. They see the same rising medical costs you do. But with limited resources, they're allocating budgets across multiple teams—product development, sales expansion, talent acquisition, operations. A ₹9-15 lakh increase in benefits spend competes directly with those priorities.

Super Top-up changes the conversation entirely. Instead of asking finance to choose between employee health coverage and other critical investments, you're offering a solution that ticks every box:

✓ Employees get comprehensive coverage (₹8-10 lakh total protection)

✓ At pricing they can't access individually (40-50% below market rates)

✓ With zero additional cost to the company (employee-funded, company-facilitated)

✓ And minimal administrative effort (one invoice, payroll deduction for reimbursement)

It's not "HR wants more budget and finance says no."

It's "let's work together to solve a real problem without competing for limited resources."

That's what Super Top-up does. It helps employees access group pricing they can't get on their own, while letting finance allocate budgets where they're needed most.